Table of Contents

Introduction

Have you ever wondered how much those credit card interest rates could be costing you over time? Whether you’re trying to pay off an existing balance or considering applying for a new credit card, understanding and comparing interest rates is one of the smartest financial moves you can make. Every percentage point can add up to hundreds or even thousands of dollars in interest payments, affecting your financial freedom more than you might realize.

Credit cards have become an essential tool for everyday spending, emergencies, and even building credit history. However, the convenience of credit can come with costly interest charges if the balances aren’t managed carefully. Millions of consumers carry balances month to month, often unaware of how different interest rates can sharply impact the amount they pay. This makes the ability to compare credit card interest rates not just useful but vital for anyone looking to save money and make informed borrowing decisions.

Statistics show that the average credit card interest rate hovers around 16% to 24% APR depending on creditworthiness and market conditions. Carrying a balance on a high-interest card can quickly erode your finances, especially if payments are minimal or late. Financial experts emphasize the importance of shopping around and understanding the fine print when selecting a credit card. This way, you can avoid unexpected costs and choose a card tailored to your financial habits and goals.

Beyond just the numbers, there’s an emotional aspect as well. Struggling with credit card debt or feeling overwhelmed by monthly interest charges can lead to stress and anxiety. On the flip side, acquiring the knowledge to choose the best interest rates empowers you to regain control, reduce financial pressure, and enhance your overall well-being. If you’re new to credit cards or want to sharpen your financial skills, you might want to start by learning how to read a credit card statement. Understanding this important document is key to managing your credit effectively and spotting interest charges you might want to avoid.

Interest rates are just one part of the bigger picture, but they play a crucial role in your total credit costs. Many people also wonder about ways to lower or altogether avoid these interest charges. If reducing interest payments is a priority, consider exploring practical advice on how to avoid credit card interest charges. These actionable tips can save you money and help you develop healthy credit habits for the long term.

What You’ll Learn in This Guide

In this comprehensive guide, we’ll help you navigate the complex world of credit card interest rates so you can make confident decisions. Here’s what we’ll cover to give you a well-rounded understanding:

- Understanding Credit Card Interest Rates: You’ll learn what interest rates really mean, how they are calculated, and why understanding the different types of rates like purchase, balance transfer, and penalty APR matters.

- How to Compare Credit Card Interest Rates Effectively: We’ll walk you through key factors to look out for when comparing cards, including introductory offers, fees, and the standard APR after introductory periods.

- Factors That Influence Credit Card Interest Rates: Discover how your credit score, economic conditions, and issuer policies can affect the rates you qualify for, and simple ways to improve your creditworthiness.

- Strategies to Manage and Minimize Interest Costs: Learn practical tips to reduce interest charges like paying balances in full, timing payments right, leveraging balance transfers, and negotiating with card issuers.

Throughout this guide, we will share actionable insights as well as helpful resources to sharpen your financial decision-making skills. We’ll also explore common pitfalls to avoid and how to use comparison tools and calculators to simplify your search for the best credit card option.

Coming up, you’ll dive deeper into the mechanics of how credit card interest rates work, including the daily periodic rate and average daily balance method. We’ll break down the different types of APRs you should be aware of so you can read the fine print like a pro. Next, you’ll see how to effectively compare cards based on interest rates and associated costs, ensuring you spot the best deals in the market.

We will also discuss important factors that impact interest rates beyond just your credit score, such as market trends and policies set by the card issuers. Finally, we’ll provide proven strategies for managing and minimizing your interest costs, helping you keep more money in your pocket and maintain healthier credit habits.

By the end of this guide, you’ll be equipped with the knowledge and tools needed to choose the best credit card interest rate for your unique financial situation. Armed with this information, you can make smarter, more cost-effective choices that boost your financial confidence and security. Let’s get started on your journey to mastering credit card interest rates and unlocking better financial opportunities.

Choosing the right credit card involves more than just looking at the surface rewards or card design; understanding and comparing credit card interest rates is essential to making an informed decision that can save substantial money over time. Interest rates affect how much you pay when you carry a balance, making it critical to fully grasp how these rates work, the types involved, and effective comparison strategies. This discussion delves deeply into the nuances of credit card interest rates, helping you become confident in evaluating cards based on their costs and aligning your choice with your spending and repayment habits.

Understanding Credit Card Interest Rates and Their Impact

Credit card interest rates represent the cost of borrowing money when you do not pay your full statement balance by the due date. These rates are expressed as Annual Percentage Rates (APR) and apply differently based on the type of transaction or card agreement. They serve as a fundamental factor in the total cost of using credit, thus understanding how rates are determined and applied helps you manage expenses and avoid surprise charges. For those new to credit or seeking to deepen their knowledge, it helps to review the basics of how to read a credit card statement, which detail how interest appears and accumulates on your monthly bills.

Interest is not a single flat rate but varies by transaction type, duration, and card issuer policies. Knowing this allows you to spot opportunities for savings, like taking advantage of introductory rates or negotiating better terms. It also encourages disciplined usage behavior that aligns with financial goals. By fully understanding these elements, you can better anticipate the costs and make choices that fit your lifestyle, whether you use your card mainly for convenience or financing larger purchases.

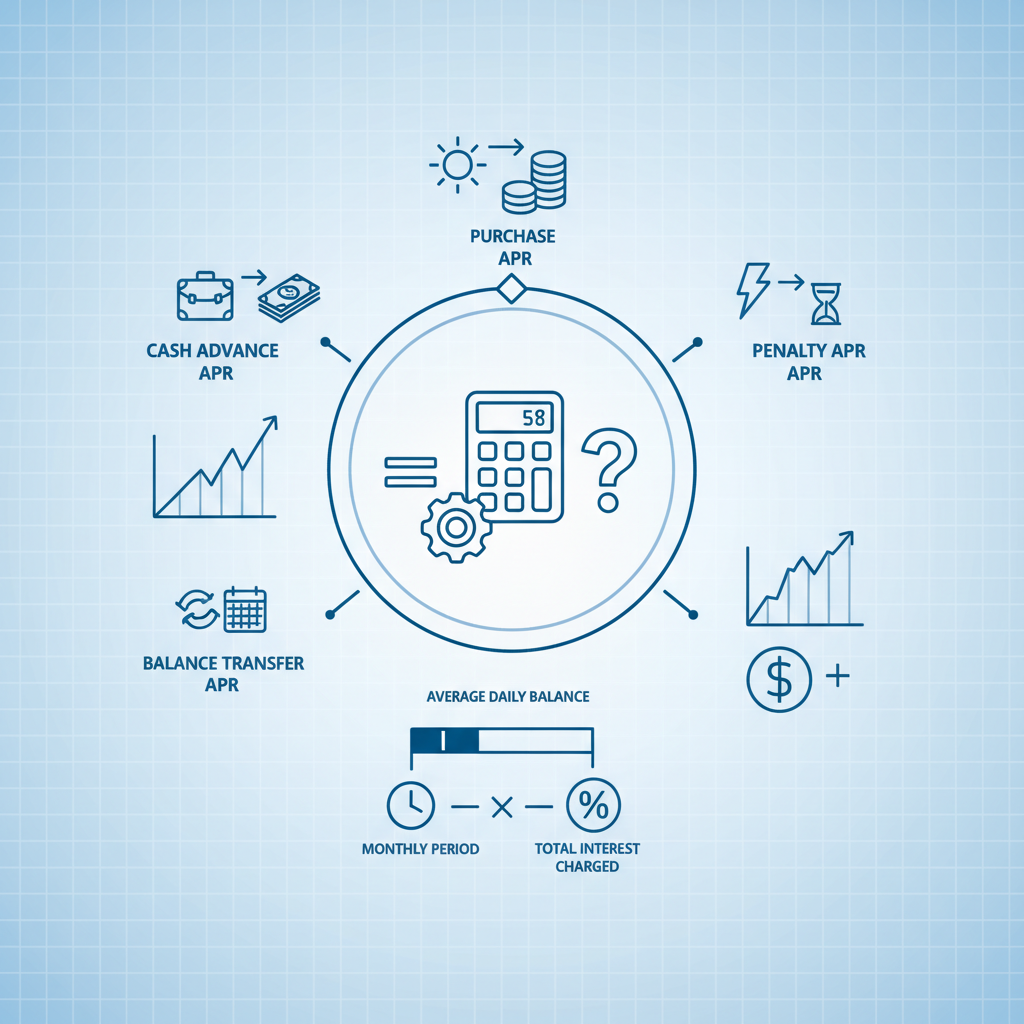

Key Features of Credit Card Interest Rates

When exploring credit card interest, several core elements deserve focus to comprehend the rate structure and its effects thoroughly:

- Purchase APR: This rate applies to everyday purchases like groceries, gas, and online shopping. It is typically the main APR affecting most card users and determines ongoing cost if balances are carried month to month.

- Balance Transfer APR: Many cards offer a different rate on balances transferred from other cards, sometimes with a promotional low or 0% introductory period. Understanding the terms of this APR is crucial for optimizing savings during debt consolidation.

- Cash Advance APR: Cash advances often carry a higher APR than purchases, reflecting the increased risk and immediate access to cash. These transactions also usually start accruing interest immediately without a grace period.

- Penalty APR: If you miss payments or violate terms, a penalty APR may kick in, significantly increasing your interest rate. Awareness and avoidance of penalty triggers are vital for maintaining manageable credit costs.

How to Compare Credit Card Interest Rates Effectively

Simply spotting the APR numbers on credit card offers does not provide the full picture. Comparing credit card interest rates requires digging into the fine print, understanding the timing and duration of rates, and the fees and conditions attached. Many consumers overlook the impact of introductory offers expiring or fail to notice penalty increases and annual fees combined with interest costs. By learning to read fine print and evaluate terms fully, you make a well-rounded assessment that matches your financial needs.

Additionally, leveraging comparison tools like online calculators and reputable comparison websites enhances your ability to visualize potential costs under various scenarios. These tools help anticipate how rates translate into monthly payments and total costs over time. For those wanting to optimize their decision-making process, exploring how to avoid credit card interest charges offers practical strategies that complement interest rate shopping.

Key Considerations When Comparing Rates

Performing a thorough comparison involves evaluating these core aspects beyond just the headline APR:

- Introductory Rates and Terms: Understand the length and conditions of promotional rates. Check if balance transfers or purchases have different introductory periods and what happens once the period ends.

- Standard APR After Introductory Period: Know the ongoing rate that applies post-promotion. This is the rate you will likely pay if you carry balances long term, so it must be affordable and competitive.

- Fees and Penalty Rates: Identify any annual fees, late payment fees, and penalty APRs. Sometimes a card with a slightly higher APR but no fees may cost less overall depending on usage patterns.

- Comparison Tools: Use online calculators and comparison sites to simulate borrowing scenarios and visualize how different rates impact payments and interest costs over time.

Conclusion

Understanding and comparing credit card interest rates is crucial for anyone looking to manage their finances effectively and avoid unnecessary expenses. Throughout this guide, we’ve explored the different types of credit card APRs including purchase APR, balance transfer APR, cash advance APR, and penalty APR. Each type serves a distinct purpose and carries its own implications on how much interest you might be charged. By knowing these categories, you can better evaluate which card aligns with your spending habits and financial goals.

The method of interest calculation, often using the daily periodic rate and the average daily balance, plays a significant role in how much you ultimately owe. This reinforces the importance of not just looking at the APR, but also understanding how interest accrues over time. Additionally, various factors impact the interest rates you qualify for, such as your credit score, current economic conditions, and issuer-specific policies. A higher credit score generally leads to more favorable rates, and being mindful of market trends can help you time your applications or requests for better terms.

Managing and minimizing these interest costs requires proactive steps. Paying your balances in full each month is the most effective way to avoid interest charges altogether. If carrying a balance is necessary, making payments on time and as frequently as possible can reduce the principal and lessen interest accumulation. Another smart strategy involves utilizing balance transfer offers to move debt onto cards with lower rates, thereby saving money on interest payments. For those carrying balances regularly, it may also be worthwhile to communicate with your card issuer to negotiate better terms or potentially lower rates based on your payment history and creditworthiness.

To get started on effectively managing your credit, consider learning how to read a credit card statement. This knowledge is indispensable in tracking your spending, spotting fees, and understanding how interest is applied to your account. Furthermore, practical advice on how to avoid credit card interest charges can provide you with actionable tips that help you maintain healthier credit habits and save money in the long run.

Choosing the best card with a suitable interest rate is more than just finding the lowest number—it’s about understanding the full picture including fees, reward programs, and your personal financial situation. By approaching your credit card selection with informed caution and ongoing management, you empower yourself to reduce financial stress and improve your overall economic health.

Ultimately, gaining mastery over credit card interest rates gives you greater control over your money. It allows you to make credit work for you rather than becoming a source of debt and anxiety. With the tools and insights you’ve gained, you can confidently make choices that foster long-term financial stability and freedom. Remember, knowledge is power—so keep educating yourself and stay proactive to achieve the best outcomes with your credit cards.